At Misión Verdad we have kept track of the negative effects of unilateral coercive measures (UCM) [aka US blockade] on Venezuela, and more specifically, their harmful consequences on the main company that provides oil revenues to Venezuela, Petróleos de Venezuela, SA (PDVSA).

All the reports and papers issued by organizations or individuals that are not binding on each other, but have Venezuela in their focus, provide a clear conclusion regarding the effects of the US blockade on the local economy: each aggression against PDVSA, through executive orders issued by the current US administration, has notably hit the country’s crude production, thus generating significant damage to sensitive areas throughout the Venezuelan economic apparatus.

We will go on to comment on one of those papers. On this occasion, the anti-Chavista economist Francisco Rodríguez made a report on the repercussions of UCM on oil production in the Orinoco Oil Belt, commenting in his work that financial and oil “sanctions” fueled huge losses in production of oil in that strategic geographic area.

Below we display some of the most outstanding data.

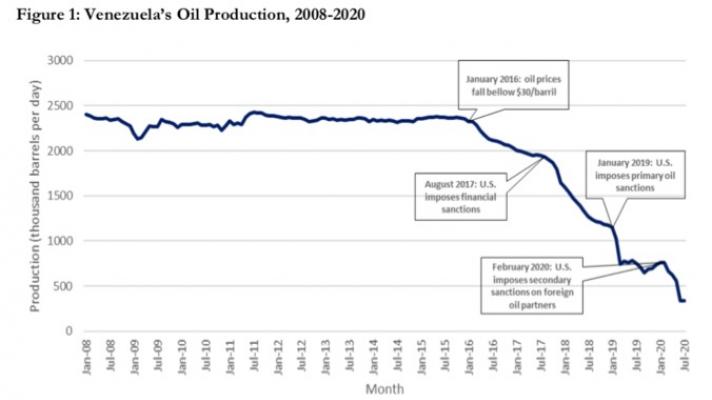

1. Production started to fall in 2016

Perform his own calculations based on OPEC data, Rodríguez points out that production stability was recorded until 2016, when the effects of low global crude oil prices provoked a slight decline.

However, the accelerated decline began in 2017, when the first direct US attack took place in the financial field. In this section, Rodríguez refers to Executive Order 13808 signed by Donald Trump in August 2017.

This executive order issued targeted “sanctions” with operations specifically prohibited for US citizens, and operations carried out in the United States with the primary objective of attacking operations of a financial nature that involved PDVSA.

In the investigation, Rodríguez recalls that, before the imposition of “sanctions,” PDVSA had begun to refinance a significant part of its arrears with service providers through the issuance of promissory notes under New York law and concludes that Executive Order (EO) 13808 put an end to these types of agreements, prohibiting the payment of the debt to any creditor qualified as a “person in the United States” by the EO.

Rodríguez points out that, as of mid-2017, PDVSA was keeping up with at least $3.2 billion of notes with General Electric, Halliburton and Schlumberger, but the UCM prevented PDVSA from issuing new notes and holders from negotiating them.

Although there is the option of OFAC licenses, this alternate mechanism has little or almost no effectiveness, as was exposed in the review by the Government Accountability Office of the United States (GAO), previously outlined by Misión Verdad. The aforementioned mechanism produced, according to Rodríguez, large losses for the companies that had agreed to refinance the debt with PDVSA.

However, Chevron is the only US company in the oil sector, on Venezuelan territory, that was granted licenses together with other US companies to continue operating in Venezuela from the beginning of the UCM. This was not the case for European companies such as Repsol and ENI.

On another front of analysis, the economist mentions that production also suffered a greater fall in 2019 with the application of secondary “sanctions” for oil-related activities. This data on “secondary sanctions” is crucial for mapping the resurgence of the unilateral attack on PDVSA. In “sanctioning” jargon, secondary sanctions are designed to dissuade non-US citizens from changing their minds in doing commercial and financial transactions with PDVSA.

In other words, this type of UCM essentially operates by restricting the access of a non-US person to the capital market or to the US banking system, if said person becomes involved with PDVSA.

With this we refer to the fact that in the Orinoco “Hugo Chávez” Oil Belt, cooperation agreements were signed with a wide list of companies, such as Rosneft, Repsol, ONGC, Oil India Limited, Indian Oil Corporation, Chevron, INPEX, and Mitsubishi, to name a few. In this way, all of them were harmed by carrying out or continuing oil operations in Venezuela.

Rodríguez argues that there are several reasons why financial “sanctions” led to a much worse trajectory of the country’s oil industry than if Venezuela had experienced a scenario without UCM. One of them is presented in the next section.

2. The reserves of the Orinoco Oil Belt

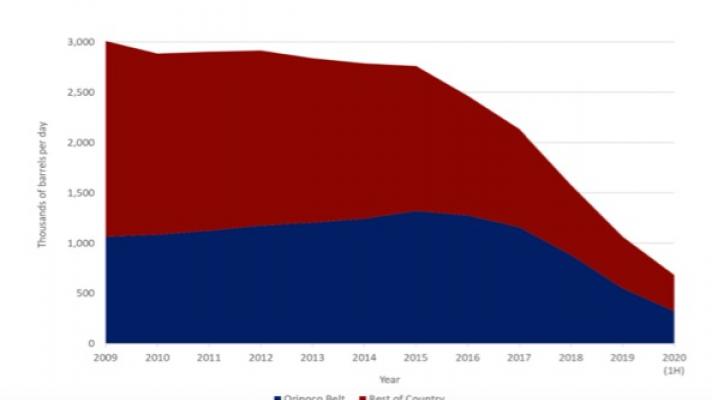

The Orinoco Oil Belt was nationalized in 2007 by then-President Hugo Chávez. It is made up of four large oil fields in which more than 20 foreign companies were commercially and operationally involved, becoming the geostrategic oil heart of the country.

In Rodríguez’s research, a graph of the production of the Belt shows a production growth between 2009 and 2015. Even with the general production decline set by this economist in the previous section, with the drop in prices in 2016, the Belt’s production remained stable until August 2017, when the pronounced drop in this area of exploitation began.

According to the figures managed by Rodríguez, from August 2017 to 2020 the production of mixed companies decreased by 90.1%, a rate slightly higher than that registered in fields that were the exclusive property of PDVSA (86.9%).

This is linked to what was previously explained about secondary “sanctions.” For instance, in 2020 the administration of Donald Trump imposed UCM on the Russian subsidiary Rosneft Trading for maintaining commercial ties with the constitutional government of Nicolás Maduro, meaning PDVSA.

In short, crude oil production in the country experienced a serious decline, both in the fields operated entirely by PDVSA and in those controlled by joint ventures with international and private partners.

For 2012, President Hugo Chávez reported that, on average, slightly more than one million barrels a day were produced in the Belt, and it was expected, by the middle of that year, to increase to one and a half million, since the plan in this extensive territory of hydrocarbon drilling was to reach, by the year 2019, four million barrels per day. The calculations, investments, and the plan per se were clear and feasible, but the illegal coercion imposed by the United States on the sector led to the hampering of immediate development goals in Venezuela.

Keys to the conclusion of the investigation

Rodríguez and his team used financial and economic calculations to corroborate their hypotheses on the effects of the “sanctions” on the country’s oil sector. Using differential access to credit from oil companies in the Orinoco Oil Belt, the Venezuelan economist points out the following:

• The lack of access to the credit market caused by the “sanctions” may explain between 45.4% and 61.7% of the drop in production observed in the region encompassed by the Belt.

• Their estimates suggest that in the absence of UCM on the oil sector, Venezuela’s oil exports could be roughly two to three times larger than their current levels.

• Financial and oil “sanctions” caused large losses in oil production among companies that had special financing agreements that allowed access to credit, compared to those that did not. In short, these companies [the former] experienced a drop in production of about half, following the approval of US measures.

• By excluding other companies from the possibility of gaining access to similar agreements, Rodríguez argues that the “sanctions” prevented the adoption of policies that, if implemented, would have ensured the stability of the Belt’s production.

• Washington’s financial provisions acted as an economic surgical attack capable of replicating the effects of a full-blown trade embargo.

It is pertinent to point out that, despite the fact that in 2017 “sanctions” were imposed on US actors or companies that proceeded to initiate or maintain commercial and financial ties with PDVSA, this maneuver had an impact on other international players because they, under that threat, faced the possibility of being blacklisted, and facing a series of penalties if the “Trump Decree” was violated.

This type of EO is issued under the provisions of the [US] International Emergency Economic Powers Act (IEEPA). Likewise, since 2014, the Venezuela Defense of Human Rights and Civil Society Act paved the way for all UCM imposed against Venezuela.

So if violating the IEEPA can lead to fines of up to $1 million per violation, which international company would take this kind of risk? Even if an ordinary person tried to negotiate with PDVSA, they could face 20 years in prison, according to the aforementioned law.

Taking into account the results of Rodríguez’s analysis, new evidence is added to the extensive list of the major impacts of the UCM on Venezuela’s oil sector that undoubtedly affected the country’s economy, as has been denounced for years.

Rodríguez comments that the financing agreements for PDVSA proved to be successful between 2013 and 2017. Therefore, the crucial blow was directed at the attractive core of the Belt: affecting the financing and negotiation agreements that, as well as with Petrocaribe, were unmatched in the region’s oil business sphere.

The deprivation of access to the world’s capital and financial markets led to a notable dent in the country’s oil production, thus rupturing Venezuela’s export capacity to different partners in the world [and affecting basic human rights for millions of Venezuelans].

Translation: Orinoco Tribune