In recent weeks, the information trend in economic matters has been led by multiple geopolitical endeavors that point towards de-dollarization or the diversification of finance and the world economy. It is becoming evident that a transformation of the financial system is being forged with the intention to decentralize the dollar rather than eliminate it from the overall equation, a move led by large emerging powers.

In the case of Latin America, two events showed important signs of such a financial transformation since they came from the countries that represent the largest economies in the south of the Latin American region:

- The recent agreement on financial transactions in national currencies between Brazil and China;

- The statements by Argentinian Minister of Economy Sergio Massa on the use of the swap agreement between the central banks of China and Argentina concerning investments and payments using the Chinese yuan.

Although these facts embody an important and outstanding financial step in the international spectrum, other variables show the real probability that de-dollarization in the region may materialize in the not-too-long term.

In order to see where Latin America stands in this regard, three approximate elements are taken into account: commercial exchange in other currencies; monetary reserves; and the exchange platform, where the SWIFT system currently sets the standard.

Beyond the agreements through the swap mechanism, the variable of monetary reserves indicates another behavior.

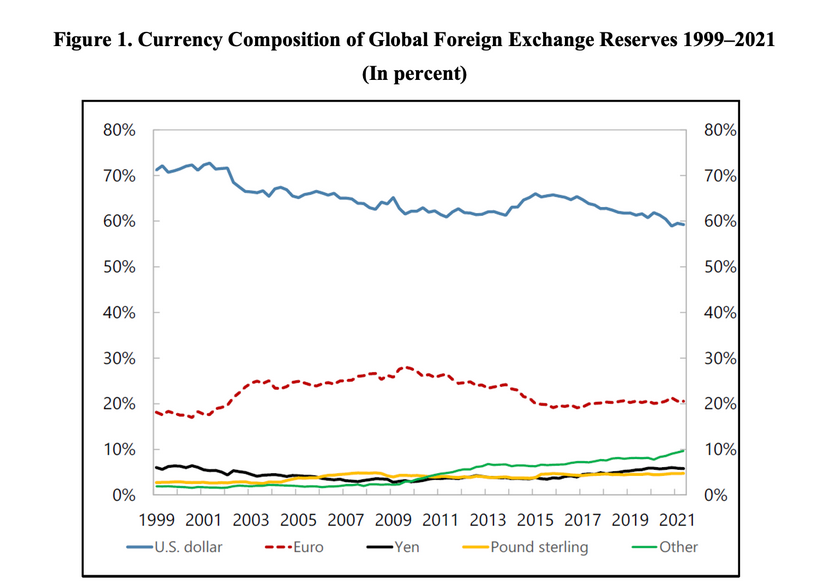

The International Monetary Fund (IMF) released a report in 2022 titled “The Stealth Erosion of Dollar Dominance: Active Diversifiers and the Rise of Nontraditional Reserve Currencies,” stating that despite a reduction in the dollar’s share of central bank reserves since 2000, the currency continues to account for the largest share of reserves, followed by the euro, while the yuan—intentionally—was grouped in a green “other” line, as can be seen below in Figure 1.

In the report, they point out that “this decline [of the dollar] reflects active portfolio diversification by central bank reserve managers… the shift out of dollars has been in two directions: a quarter towards into the Chinese renminbi [yuan] and three quarters into the currencies of smaller countries.”

On a global scale, the dollar’s participation in terms of monetary reserves in the last 20 years has been above 50%, a considerable figure in relation to the times of change in its hegemony.

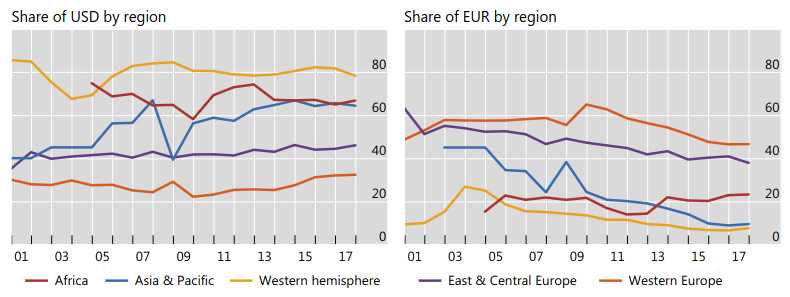

According to the Bank for International Settlements (BIS), from 2001 to 2017, international reserves by region show the distribution of currencies: greater participation of the dollar in Latin America and Canada (Western Hemisphere for the BIS), followed by Africa and Asia. On the contrary, the participation of the euro is high for the countries of Europe, as is to be expected.

From a historical perspective, high levels of inflation, depreciation of the local currency, and chronic monetary financing from institutions such as the IMF that caused dollar-denominated budget deficits in most of Latin America during the 1980s and 1990s led to the dollar dominating the various financial issues in the region, making it one of the most dollarized regions in the world.

This was reflected in 2005: a study by the Inter-American Development Bank indicated that, on average, in non-Latin American emerging markets, “the share of dollar-denominated deposits and loans was around 22% and 19% respectively, in Latin America the average figures are closer to 37% and 40%.”

So, based on the previously mentioned elements, especially with the monetary reserves around the world, the fulcrum is the dollar by a wide margin. In addition, the SWIFT exchange platform has had no competition until now, being a key bridge to carry out the exchange and international payments.

However, the dynamics with international trade, mainly under the swap logic, make more sense when seeing results. China is the largest market in the world, and its financing capacity is currently unmatched, making the yuan gradually internationalize year after year from this front.

In this sense, the swap agreements with China are the most outstanding in this circuit in relation to Latin America. After the financial crisis of 2008, countries such as Brazil, Argentina and Chile signed the first swap agreements with China, giving significant results in financial and trade relations. The renewal of these agreements took place in 2013-2014. This year, Brazil and Argentina resume them again.

This can be better visualized in Misión Verdad’s general study on China’s exports and imports in the region, serving as a visual of this premise and is referenced below.

It is too soon to equate the internationalization of the yuan with the dollar, knowing that China does not seek to replace the US currency with its own but instead wants to carve out a space in the international financial portfolio. This intention was made clear by Zhou Xiaochuan, then-governor of the People’s Bank of China, in a 2009 report pointing out that the financial crisis showed the dangers of relying on one nation’s currency, meaning the dollar, for international payments.

It can be inferred that these swap operations, primarily using the yuan, are maneuvers that aim to alleviate the outflow of US dollars.

One of the most advanced initiatives was in 2009 when four ALBA-TCP members: Bolivia, Cuba, Ecuador and Venezuela, launched their own compensation mechanism, the Unified Payment Compensation System (Unified System of Regional Payment Compensation, SUCRE). It served as a notorious boost in the face of foreign exchange shortages. However, apart from the fact that it was not the entire region but a small block, its disadvantages lie in limitations on intra-regional trade and the financial and liquidity capacity of the region’s central banks.

Latin America could take leaps and bounds in this matter if it managed to establish a regional unit of account that could allow the interoperability of payments between countries with national currencies that could transform into a common currency in the long term. In this way, the region could immerse itself in the financial transformation advancing worldwide in terms of global monetary diversification.

Although the region has not been able to integrate politically in a lasting way as Africa has done with the African Union, it has also been unable to define tangible paths in the commercial sphere. This is because the establishment of a common currency is far from being achieved, an option that can clear the path towards its integration in the global commercial realignment of our days, a consequence of current geopolitical events.

It is known that the de-dollarization process is gradual. However, the region must rise to the challenge without ambiguity. This is the moment. There must be political will that gives meaning and direction to the initiative.

Translated by Orinoco Tribune.